If you run a dental clinic in Dubai, you already know that insurance is not just a billing issue—it is a clinical, operational, and compliance challenge all wrapped into one. Between verifying patient eligibility, navigating pre-authorisation requirements, submitting claims through eClaimLink, and managing a wave of rejections that arrive with frustratingly little explanation, it can feel like your front desk is fighting a second job just to get paid.

But the clinics that understand how dental insurance really works in Dubai—not just the theory, but the day-to-day mechanics—are the ones that collect faster, deny less, and spend more time focused on patient care.

This guide is written specifically for clinic owners, practice managers, and insurance coordinators who want a practical, honest breakdown of coverage structures, the claim submission workflow, common denial reasons, and how to build a process that works. Let’s get into it.

The Dental Insurance Landscape in Dubai: What You Need to Know First

Dubai operates under a mandatory health insurance framework governed by the Dubai Health Authority (DHA). However, it is crucial for clinics to understand one important distinction: dental care is not automatically included in the minimum essential benefits required under the Essential Benefits Plan (EBP).

The EBP, which was designed to cover lower-income workers, includes only basic emergency dental treatment. Comprehensive dental coverage—including routine checkups, fillings, root canals, crowns, orthodontics, and implants—is typically offered as an add-on benefit, available in mid-tier and premium insurance packages offered by providers such as Daman, AXA Gulf, Sukoon (formerly Oman Insurance), Neuron, and others.

This means that not every patient walking into your clinic with an insurance card is covered for what they need. As a clinic, you are the first line of defence against uncovered treatments being performed without a patient’s financial consent. This is not just good practice—it is a regulatory expectation.

Understanding the insurance landscape in Dubai also means knowing your payer mix. Most dental clinics in Dubai deal with a combination of:

- Corporate group plans (large employer schemes covering employees and sometimes their dependents)

- Individual health plans (privately purchased policies with varying dental riders)

- Government employee schemes (for public sector workers, managed by Daman under the Thiqa plan for UAE nationals and the Basic plan for expatriate government employees)

Each of these payer categories has its own rules, pre-authorisation thresholds, covered procedure lists, and claim submission timelines. One of the biggest mistakes a clinic can make is applying a one-size-fits-all approach to insurance when each insurer—and sometimes each plan within the same insurer—behaves differently.

What Is and Is Not Typically Covered

One of the most common pain points for dental clinics in Dubai is managing patient expectations when their plan does not cover what they expected. A proactive clinic explains this upfront. Here is a general breakdown of how coverage tends to be structured:

Typically Covered (with co-payment)

- Dental examinations and consultations

- Dental X-rays (periapical, bitewing, panoramic)

- Scaling and polishing (prophylaxis), usually once or twice per year

- Simple extractions

- Basic restorations (amalgam and composite fillings)

- Pulpotomy (nerve treatment for primary teeth)

- Root canal treatment on anterior and premolar teeth (posterior RCT may require prior authorisation)

- Stainless steel crowns (for paediatric patients)

Covered Under Premium Plans or With Prior Authorisation

- Root canal treatment on molar teeth

- Porcelain-fused-to-metal (PFM) or zirconia crowns

- Fixed bridges

- Full or partial dentures

- Orthodontic treatment (often with an annual or lifetime maximum limit, and a waiting period of 6–12 months)

- Surgical extractions and minor oral surgery

Typically Excluded

- Dental implants (explicitly excluded in the majority of plans)

- Cosmetic procedures: tooth whitening, composite bonding for aesthetic purposes, veneers

- Teeth jewellery and other elective aesthetic work

- Treatment of pre-existing conditions (during waiting periods)

- Treatment resulting from self-inflicted injury or negligence

- Replacement of lost or stolen prosthetics

The lesson for clinics here is clear: never assume. Always verify. A patient’s card confirming dental coverage does not tell you which procedures are covered, at what percentage, and whether a prior authorisation is needed before treatment begins.

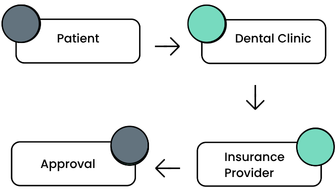

The Insurance Claim Workflow: Step by Step

For a dental clinic operating in Dubai, every insurance case involves a sequence of steps. Missing any one of them increases the risk of denial or delayed reimbursement. Here is how a well-run workflow should look.

Step 1: Patient Registration and Insurance Verification

When a new patient arrives, your front desk should collect their insurance card and Emirates ID. Beyond scanning or photographing the card, your team needs to verify:

- Active coverage status: Is the policy current and not lapsed?

- Network type: Is your clinic on the insurer’s network? Are you an “in-network” provider for this specific plan?

- Dental rider: Does the policy include dental benefits, or is it medical-only?

- Waiting period: Has the patient recently joined this plan and is still within the waiting period for certain dental services?

- Annual maximum: How much of the annual dental limit has already been consumed?

- Co-payment percentage: What portion will the patient be responsible for paying at the point of service?

Many insurers in the UAE provide online eligibility portals or have integrated eligibility check APIs. In Dubai, the eClaimLink system (operated through the DHA) also provides an eligibility check function that should be the standard starting point for verification. A DHA-certified clinic management system like Balsam Medico can pull this data directly, reducing manual entry errors.

Step 2: Treatment Planning and Cost Estimation

Once eligibility is confirmed, and before treatment begins, your dental team should document:

- The patient’s chief complaint

- Clinical examination findings

- Diagnosis codes (ICD-10-AM format, as required by the DHA)

- Proposed treatment with corresponding CDT (Current Dental Terminology) codes

- Estimated costs per procedure

For multi-appointment or high-value treatment plans, this documentation forms the basis of a pre-authorisation request. Presenting the patient with a cost breakdown—clearly distinguishing the insurer-covered portion from their co-payment—is both good practice and a way to avoid billing disputes later.

Step 3: Prior Authorisation (Where Required)

Prior authorisation (PA), also referred to as pre-authorisation or pre-approval, is mandatory for a growing number of dental procedures in the UAE. As of 2025, most insurers require PA for:

- Root canal treatments on molar teeth

- Crowns and bridges (especially those involving laboratory work)

- Orthodontic treatment

- Surgical extractions

- Any procedure where the estimated cost exceeds AED 1,000 per appointment

Submitting a PA request through eClaimLink requires:

- The patient’s insurance details and Emirates ID

- ICD-10-AM diagnosis codes

- CDT procedure codes

- Radiographs (attached as digital files)

- Clinical notes supporting the necessity of the treatment

- Periodontal charts (for periodontal procedures)

- In some cases, photographs (pre-treatment)

One important note for clinics: a PA approval is not a guarantee of full payment. It is an approval that the treatment is considered medically necessary and eligible for claim submission—but the final reimbursement can still be reduced or denied if the submitted claim contains discrepancies or incorrect documentation. Communicate this clearly with your patients.

Step 4: Claim Submission via eClaimLink

Dubai’s DHA requires all dental claim submissions to be made electronically through eClaimLink. Manual claims or paper submissions are no longer accepted for in-network providers. If your clinic is using a non-integrated or non-DHA-certified system, you are operating at a significant disadvantage—and a compliance risk.

A complete claim submission includes:

- Patient demographics (matching the insurance records exactly)

- Provider and facility licence numbers

- Diagnosis codes (ICD-10-AM)

- Procedure codes (CDT)

- Fees and quantities for each item billed

- Supporting clinical attachments (X-rays, treatment notes, lab reports)

- Prior authorisation reference number (where applicable)

The claim must be structured in the HL7 FHIR-compliant XML format required by eClaimLink. Systems like Balsam Medico generate this format automatically, reducing the chance of structural errors that cause batch rejections before the claim is even reviewed.

Step 5: Claim Tracking and Follow-Up

Once submitted, claims go through a review process at the insurer’s end. The typical processing timeline in Dubai is:

- Straightforward claims with no PA: 5–10 business days

- Claims requiring manual review: 15–30 business days

- Disputed or escalated claims: Up to 45 business days

Clinics should have a dedicated person or system tracking the status of all submitted claims. Live claim dashboards—available in DHA-integrated EMR platforms—let you monitor which claims are under review, which have been partially approved, and which have been denied.

Do not wait for the insurer to contact you. Build a proactive follow-up schedule into your workflow.

Why Claims Get Denied (and What to Do About It)

Denials are not random. Most of them are predictable and preventable. Here are the most common denial reasons encountered by dental clinics in Dubai, and how to address them.

1. Incorrect or Mismatched Codes

Using outdated CDT codes, applying an incorrect ICD-10-AM diagnosis code, or mismatching the procedure code to the clinical notes are among the top reasons for rejection. This often happens when a clinic relies on outdated code lists or manual coding without validation checks.

Fix: Use a system that updates CDT and ICD-10 codes automatically and validates codes against insurer-specific coverage lists before submission.

2. Missing Prior Authorisation

Submitting a claim for a procedure that required PA—but was performed without getting one—almost always results in denial. Insurers are strict about this, and retroactive PA approvals are rarely granted.

Fix: Build a PA checklist into your treatment planning workflow. If the PA is pending, delay treatment until approval is received.

3. Cosmetic vs. Medical Necessity Determination

Insurers will deny claims where a procedure is considered cosmetic rather than medically necessary. For example, a composite veneer placed for aesthetic reasons is cosmetic. The same material used to restore a fractured anterior tooth is medical. The difference lies entirely in your documentation.

Fix: Ensure that clinical notes clearly describe the clinical indication, not just the procedure. If a procedure could be perceived as cosmetic, document the medical necessity explicitly and include supporting radiographs or photographs.

4. Duplicate Claim Submissions

Submitting the same claim more than once—sometimes unintentionally, as a “follow-up” when the original is still under review—triggers automatic rejection.

Fix: Track all submitted claims by reference number. Before resubmitting, confirm the original status. Only resubmit if the original was formally rejected, not just pending.

5. Patient Not Eligible at Time of Service

If a patient’s policy had lapsed, was on hold, or the patient had not yet served their waiting period at the time of treatment, the claim will be denied retroactively—even if the insurance card appeared valid.

Fix: Perform real-time eligibility verification at every visit, not just at registration. A patient who was covered last month may not be covered this month.

6. Exceeded Annual Benefit Maximum

Once a patient has consumed their annual dental maximum, further claims will be denied until the policy renews. In Dubai, most group plans run on a calendar year basis (January to December), though employer scheme dates can vary.

Fix: Track each patient’s consumed benefits through your system and notify them—and your clinical team—before benefits are exhausted.

Handling Rejections and Resubmissions

Every clinic will face rejections. The difference between a high-performing clinic and an average one is not the absence of rejections—it is how fast and effectively they are resolved.

When a claim is rejected, eClaimLink returns an error code and a rejection reason. These should be treated as a task list, not a dead end. Common error classifications include:

- C001 – Coding Error: A procedure or diagnosis code is incorrect or unsupported

- C002 – Missing Documentation: Required attachments are absent

- C003 – Duplicate Claim: A prior claim for the same episode of care was already submitted

- C004 – Pre-Authorisation Required: Treatment performed without prior approval

- C005 – Patient Not Eligible: Coverage was not active at the time of service

For each rejection, your team should:

- Identify the root cause using the error code

- Correct the issue (update codes, attach missing documents, obtain PA retroactively if possible)

- Resubmit within the insurer’s appeal window—typically 7 to 14 days from the date of rejection

- Document all communication related to the appeal in the patient’s file

If the rejection involves a clinical judgement call—such as a procedure being classified as cosmetic when you believe it was medically necessary—you have the right to escalate. Most insurers in the UAE have a formal appeals and grievance process. If an issue cannot be resolved with the insurer directly, and patient rights have been affected, the DHA can be approached as a regulatory escalation point.

Building a Culture of Insurance Compliance in Your Clinic

The clinics that manage insurance best do not treat it as a billing department problem. They embed insurance awareness across the entire team.

Here is what that looks like in practice:

At the front desk: Every patient is verified before treatment. Co-payments are collected at the time of service, not chased afterward. PA statuses are tracked and confirmed before the patient enters the treatment room.

In the treatment room: Dentists document findings clinically and thoroughly. They understand that what is written in the notes is what gets paid. They avoid performing procedures that are not covered without patient consent and a signed financial acknowledgement.

In the back office: Claims are submitted same day or within 24 hours of treatment. Rejections are reviewed and actioned within 48 hours. Monthly reconciliation ensures no claim falls through the cracks.

Clinic-wide: The entire team understands that insurance revenue is the backbone of cash flow, and that every step they take—from patient greeting to claim submission—contributes to it.

How Balsam Medico Simplifies Insurance for Dubai Dental Clinics

Managing dental insurance manually in Dubai is simply not sustainable. Between eClaimLink integrations, HL7-compliant claim formats, real-time eligibility checks, and the growing complexity of multi-payer environments, clinics need a system that handles the heavy lifting.

Balsam Medico is a cloud-based clinic management system built specifically for the UAE healthcare environment. It is fully integrated with eClaimLink and designed to support every step of the insurance workflow:

- Real-time eligibility verification through insurer portals and eClaimLink

- Pre-authorisation management with automated documentation checklists

- CDT and ICD-10-AM code libraries that are updated in line with DHA requirements

- One-click claim submission with HL7-compliant formatting

- Claim status dashboards for live tracking across all active submissions

- Rejected claim workflows with built-in root cause classification and resubmission support

- Benefit consumption tracking per patient, per policy year

- NABIDH and Riayati integration for UAE-wide health record compliance

Whether you are a single-chair practice or a multi-branch dental group, Balsam Medico gives your team the tools to submit cleaner claims, reduce denials, and get paid faster.

Final Thoughts

Dental insurance in Dubai is not going to get simpler—it is going to get more sophisticated. More procedures will require pre-authorisation. Digital auditing will catch more errors. Compliance expectations will rise. The clinics that invest in understanding their payer environment, building clean workflows, and using the right technology will be the ones that thrive.

The good news? The fundamentals are not complicated. Verify eligibility. Document thoroughly. Code accurately. Submit electronically. Follow up proactively. Appeal rejections with evidence.

Master those six steps, and your insurance process will stop being a source of stress and start being a source of reliable, predictable revenue.

Connect with Us

Ready to embark on this exciting journey? Contact us today:

📍 Dubai, United Arab Emirates – Tel: +971 56 640 9602

📍 Khartoum, Sudan – Tel: +249 91 273 1048

Explore Balsam Medico and discover a world of efficient clinic management at www.balsammedico.com. Together, let’s reduce fines, elevate efficiency, and embrace a new era of dental healthcare.

One last thing..

PS: We built Balsam Medico to be the best software for clinics in UAE and the middle east. It is powerful, flexible, and most importantly, very easy to use.

If you have two minutes, see how it works.

This is the main landing page to learn more.